Inflation causes your money to gradually lose value, keeping money at home or in a bank is a bad financial decision that leads to guaranteed loss of spending power. Technology developments in online brokerage firms like Fidelity has allowed the investment industry to remove barriers to entry; in fact, you can start investing with little money right now. We are going to discuss investments with little money in term savings, stocks, funds, gold and yourself.

Term savings

Saving in banks is a very popular investment, since the risk of bankruptcy is relatively small and state deposit insurance is up to $100,000, term savings are a safe way to invest. However, what about the cost-effectiveness of saving? Even in periods when interest rates are high, saving is an unprofitable way to invest.

The inflation rate is higher than the nominal interest rate most of the time. Specifically, what is the annual interest rate of 5% worth to you if the cost of living, real estate, has increased by 6-7%?

Stocks

Potentially very lucrative investments, but also risky, the more lucrative, the riskier. The prices of individual stocks can rise by several hundred percent in just a few years, it is very difficult to recognize when and which stocks will have the highest yield. The stocks are also subject to cyclical ups and downs related to good economic times and recessions, which come periodically every 2-10 years.

Stocks are companies and companies have the possibility of market loss and even bankruptcy.

Despite the high risk involved, investing in the stock market is a rewarding option that has outperformed others for a significant amount of years. Investopedia reports that stocks have typically seen a return of 10-12% overall.

Everyone wants to invest in brands we are familiar with, but companies like Apple, Google and Amazon can be hundreds, if not $1,000s for a single share.

If you want a piece of Amazon, but only have a $100, you can invest with services like Fidelity and Public with what are called “fractional shares”.

Fractional shares are a piece, or a fraction of a share, and they can be tiny, as small as one-thousandth of a share. Fidelity’s aim is to open financial services to anyone. The service will allow you buy a few fractions of Google or Amazon with your $100.

When Google goes up 10%, so will your fractions.

These firms make it easy for new users to get started investing. Public offers a social component that allows you to see what other users are investing in and ask users for advice. M1 Finance, Betterment and Stockpile are also good options.

I also like Webull for the investing community.

Dividend Stocks

Some companies that perform well on a regular basis offer a dividend to their stockholders. Even if you only buy one stock, if it’s a dividend stock, you can re-invest the dividends and buy more stock.

There are several stocks that are very reasonable and pay dividends. AT&T for example is under $40.00 a share and pays $.52 cents a share (as of February 2021). It doesn’t seem like a lot, but if you start now you can add year, over year.

Anthony Sather has a fun example for dividend stocks.

“let’s invest $1 into an average stock paying a healthy 3% dividend. Like the rest of the stock market (average), it will increase 10% per year. Going off that, we’re going to assume earnings also grows 10% a year and the dividend, to match the stock.

At first, it looks really boring.

Year 1: Worth $1, $0.03 dividend, 1 share

Now. A very important detail about this whole thing is that we are going to REINVEST every single dividend. This will allow us to buy more shares in the stock as it continues to go up.

[Since this example has the dividend growing at 10% a year in-line with the share price, we’re going to be able to buy 0.03 shares (3%) every year]

Year 2: Stock worth $1.10 (10% price growth), $0.033 dividend (10% dividend growth), 1.03 shares (last year’s dividend reinvested)

Year 3: Stock worth $1.21 (10% price growth), $0.036 dividend (10% dividend growth), 1.0609 shares (last year’s dividend reinvested)

Ah..

But you see, we are grabbing more and more shares each year. So even though in year 2 the stock is priced at $1.10, our holding is worth $1.13 since we have 1.03 shares. In year 3, we have $1.28 from 1.0609 shares.

This will become very important later.

I’m sure you don’t want to read every single year– so let me just highlight some cool milestones.

Year 5: Stock worth $1.46 (10% price growth/yr), $0.044 dividend (10% dividend growth/yr), 1.1255 shares (last year’s dividend reinvested)

Value in our portfolio: $1.65

Year 20: Stock worth $6.12 (10% price growth/yr), $0.183 dividend (10% dividend growth/yr), 1.7535 shares (last year’s dividend reinvested)

Value in our portfolio: $10.72

That’s right, we just 10x-ed our investment (the famed “10 bagger”). We turned $1 into $10. Imagine turning $10,000 into $100,000. No small feat. But we’re not done yet.

Year 40: Stock worth $41.14 (10% price growth/yr), $1.234 dividend (10% dividend growth/yr), 3.1670 shares (last year’s dividend reinvested)

Value in our portfolio: $130.31

Another 20 years passes and our investment 10x-ed again. Our original $1 turned into $100. That’d be $10,000 into $1,000,000. That’s what– 1 year, 2 years, 3 years, 5 of saving? Imagine doing that several times in your life.

That’s not even the part I’m most excited about.

With 3.1670 shares now owned, we’re getting a $3.91 annual paycheck every year (in the form of a dividend). Where else can you put in $1 (once), and get back almost $4 every single year?”

Find more of his fun tips on his site: einvestingforbeginners.com

Investment funds

Investment funds can provide higher returns than term savings. However, most investment funds fail to achieve even an average stock market return. The biggest reason is the large management fees.

For example, if a 30-year-old investor saves $100 per month. They contribute the $100 to their portfolio and keep reinvesting the dividends and interest payments. The investment earns 8% per year.

For simplicity’s sake, assume compounding takes place once per year in January.

After a 30-year period, thanks to compound returns and a small monthly contribution, their portfolio will grow to $186,253.14 (as compared to $50,313.28 without the monthly contributions). While $186,253.14 is not enough money to retire on, especially after 30 years of inflation, remember that this is just with $100 a month in contributions and returns below historical averages.

Suppose the annual return is 9%, which is closer to historical averages for a 30-year period. With a $5,000 principal investment and $100 monthly contributions, the portfolio grows to $229,907.44. If the investor is able to save $200 a month for contributions, the future value of his portfolio is $393,476.48.

Voluntary Pension Funds

Pay money into a pension fund, the advantage of this way of investing money is that a person who decides on pension funds can take out the entire amount after age 50. The funds can be endowed to family in the event of the death of the account holder.

The disadvantage of this method of investing is the same as with classic investment funds – banks will not manage your money for free.

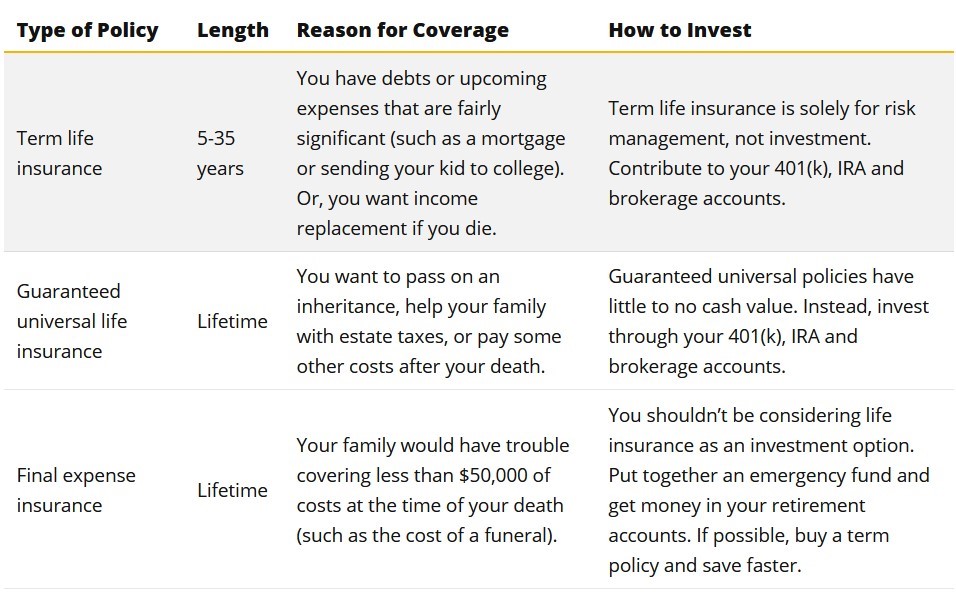

Life insurance

In addition to the principal and certain interest that the insured usually receives after the expiration of the contract, during the insurance policy the person is insured against death, injury, serious illness that requires expensive treatment and other situations agreed in the insurance policy.

The problem with insurance is that it is a long-term investment, if the insured wants to stop paying the policy after only a few years, they often don’t receive any of the funds paid in.

In case of illness, there is a risk that the insurance will not want to pay the agreed amount leading you to end up in court, which brings additional costs, dissatisfaction and stress for the insurance beneficiary. At the expiration of the insurance policy, users are often disappointed with the amount received because they see that they could have done much better by investing money in something else.

Investment gold

Investment gold is gold bars made of pure gold and gold coins with a purity of at least 90 percent, such as the Austrian gold ducats Franjo Josip. The disadvantage of owning gold is storage, it needs to be kept somewhere. Some investors in gold keep their levers at home in a hidden place, while others keep them in the safes of banks or companies specializing in the distribution and purchase of gold.

The global gold market is liquid, unlike investment funds and stocks- gold is resistant to recessions and political crises. In uncertain times, the price of gold tends to rise, bringing gold owners who choose to sell capital when it is most needed.

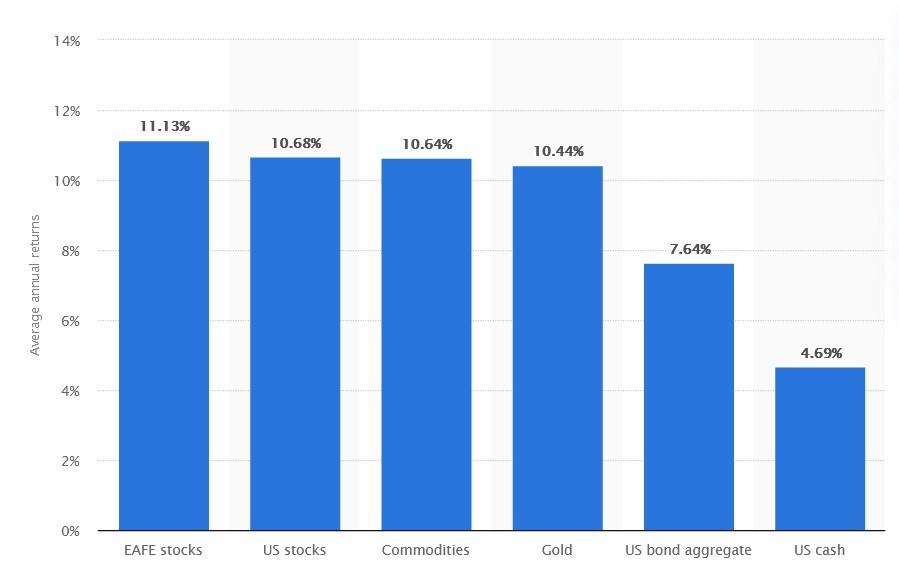

In the last 50 years, the price of gold has been growing by an average of 8 percent a year, which, in addition to covering inflation, has also brought significant profit to the sellers of gold.

Average annual return of gold and other assets worldwide from 1971 to 2019

Diamonds are certainly durable, stable in value and beautiful, but they cannot be divided at will and are not similar, gold can be divided, melted down and reconnected. Gold has been available in limited quantities and has been known throughout the world for centuries.

In times of economic and political instability, investors traditionally resort to “safe haven” for their capital, they include precious metals like gold to their investment portfolio.

The recommendation of investment advisers is that 5 to 10 percent of assets be held in gold in times of stable markets, while with the beginning of a crisis, that percentage should increase to as much as 30% of the investment portfolio. Buy before the crisis so that the price isn’t too high.

Invest in your own personal development

Reading books, taking classes for learning new skills can improve your earning power. Your $100 could turn into something much larger with the right strategy.

Studies have shown that a well written resume can make you:

- 38% more likely to be contacted by recruiters.

- 31% more likely to land an interview.

- 40% more likely to land a job.

Micro-Investment Applications

Micro-savings and micro-investment enable you to invest, but also to accumulate the money you’ll need to do it.

Probably the most popular example of a micro-savings/micro-investment app is Acorns. You can link your checking account, and each time you make a purchase, Acorns uses a process it calls “Round-Ups” to help you save money to invest.

For example, let’s say you purchase items at a grocery store for $8.25. The Acorns app will round the purchase up to an even $9.00- $8.25 will go to pay the merchant, and $0.75 will be held toward investing. Each time you accumulate $5 in round-ups, the money is transferred to your Acorns investment account.

Once there, it’s managed by the Acorns robo-advisor into a portfolio of stocks and bonds for you, then manages it by reinvesting dividends and rebalancing your portfolio to maintain target asset allocations.

As you have read, there are several options to investing, get started on one, or many of them today for your future. Subscribe for more tips and ideas.